What 30 Years of Bergen County Homeownership Actually Returns

How much wealth has a Bergen County homeowner built after 30 years? A Bergen County homeowner who purchased a single-family home for $280,000 in 1994 is sitting on a property worth $850,000–$1,100,000 today — a gross gain of $570,000 to $820,000 before transaction costs, and often more after accounting for mortgage paydown. With leverage factored in, the annualized return on initial investment has frequently exceeded the long-term stock market average.

Most people think of their home as the place they live.

The Bergen County homeowner who bought in 1992 or 1998 or 2003 and is still in that house today is sitting on something else entirely: one of the most successful investments of their lifetime, built not through financial sophistication but through the simple act of staying.

Nobody talks about this clearly. The financial press debates whether homes are good investments in abstract terms. Real estate agents discuss equity in the context of selling. Nobody sits down with a Bergen County homeowner and does the actual math — what did you put in, what did you get, and how does that compare to everything else you could have done with that money?

That's this post.

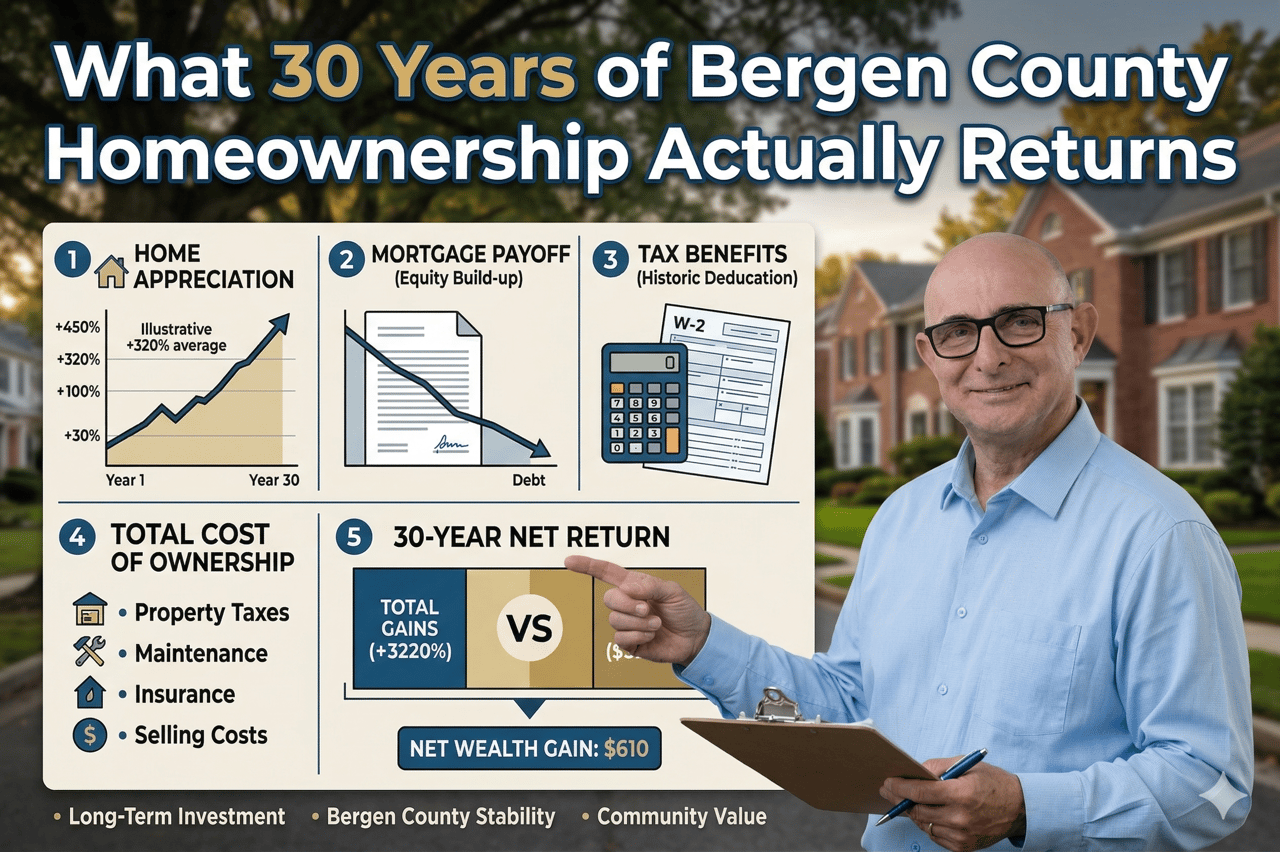

The Math on a 1994 Purchase

Let's take a specific example that reflects a realistic Bergen County transaction from the mid-1990s.

A family purchases a 4-bedroom colonial in Paramus, NJ in 1994 for $285,000. They put 20% down — $57,000 — and finance the remaining $228,000 at the prevailing 30-year fixed rate of approximately 8.5%.

Fast forward to 2025. The home's current market value is approximately $950,000, consistent with Bergen County median appreciation in established suburban towns over that period.

The gross appreciation: $950,000 minus $285,000 equals $665,000.

The return on initial cash invested: $665,000 gain on a $57,000 down payment is a gross return of approximately 1,165% — before accounting for mortgage paydown, tax benefits, or the fact that the leverage amplified returns significantly.

The mortgage is now paid off. Thirty years of payments eliminated $228,000 in debt, which adds to the net equity position.

Total net equity in 2025: Approximately $950,000 (assuming payoff, no cash-out refinancing, and typical transaction costs at sale).

The family who stayed in that house, made their payments, and did nothing particularly clever with their real estate strategy is sitting on close to a million dollars. They built that equity by living in a home in Bergen County, New Jersey.

The Leverage Advantage Nobody Explains Clearly

The reason homeownership returns look so extraordinary is leverage — and it's worth understanding precisely why.

When you buy a $285,000 home with $57,000 down, you control a $285,000 asset with $57,000 of your own money. If that asset appreciates by 10% — to $313,500 — you've gained $28,500 on a $57,000 investment. That's a 50% return on your actual cash, not 10%.

In contrast, if you invest $57,000 in the stock market and the market goes up 10%, you make $5,700. The asset base you control is only what you put in — not five times what you put in.

Real estate returns are amplified by leverage in a way that most other investments are not. And unlike margin trading in stocks — which is the stock market equivalent of leverage — residential mortgage leverage is relatively stable, tax-advantaged, and doesn't come with margin calls.

The caveat: leverage amplifies losses too. The Bergen County homeowner who bought in 2006 and sold in 2010 experienced this. The long-term owner who stayed through those cycles captured the full appreciation arc.

What the Stock Market Comparison Actually Shows

The most common benchmark for home investment returns is the S&P 500 index. Long-term S&P 500 returns have averaged approximately 10% annually before inflation, or roughly 7% after inflation.

Bergen County home appreciation since 1994 has averaged roughly 3%–5% annually in nominal terms — less than the stock market on a simple appreciation-vs.-appreciation basis.

But this comparison is incomplete for several reasons.

Leverage changes the return on invested capital dramatically. As shown above, a 5% annual appreciation on a home purchased with 20% down produces a return on initial cash investment that is much higher than 5%.

The home is tax-advantaged in multiple ways. Mortgage interest deductibility (within limits), property tax deductibility (within the SALT cap), and the primary residence capital gains exclusion — $250,000 single, $500,000 married — all reduce the effective tax burden on home investment returns compared to taxable investment accounts.

The home produces housing services. While you live in it, the home provides shelter — a consumption benefit that has real value. You are not paying rent while your asset appreciates. The stock investor earns their 10% annual return while separately paying rent. The homeowner earns their leveraged return while simultaneously living in the asset.

Nobody can live in their S&P 500 index fund. The behavioral finance literature is clear: people make better financial decisions about assets they inhabit. The Bergen County homeowner who stayed through 2008–2012 did so in part because selling meant giving up their home — not just losing on paper. That behavioral anchor, paradoxically, produced better long-term outcomes than investors who sold at the bottom of stock market cycles.

The Towns Where Returns Were Exceptional

Not all Bergen County appreciation is equal. Towns that were already desirable in the 1990s and have remained so through 2025 have produced the strongest long-term returns.

Tenafly has seen median single-family values rise from roughly $400,000–$500,000 in the late 1990s to over $1.2 million today. A 30-year hold in Tenafly is one of the strongest residential wealth-creation stories in New Jersey.

Fort Lee condos purchased in the 2000s in GWB-view buildings have appreciated significantly, with the added benefit that the Gold Coast market has continued to attract NYC-adjacent buyers willing to pay premiums for Manhattan proximity and Hudson River views.

Edgewater transformed almost entirely during this period. Properties purchased near the waterfront before the major development of the 2000s and 2010s have produced outsized returns as the town became one of the most desirable in the region.

Leonia, Englewood, and Ridgewood — towns with distinct character and long-standing residential desirability — have shown steady, durable appreciation that reflects the kind of community quality that sustains value across economic cycles.

What the Money Does Next

For the Bergen County homeowner with $600,000–$900,000 in net equity, the question is not whether the homeownership investment was successful. It clearly was. The question is what the equity does in its next chapter.

Left in the home, it earns nothing. It sits in walls and land, unavailable, while property taxes, maintenance, and carrying costs continue to accumulate.

Deployed into a Florida property in cash, it eliminates a mortgage, dramatically reduces carrying costs, and positions the family for a financially lighter second half of life. The equity trades one asset for another, but the monthly cost structure changes entirely.

Deployed into a combination of a smaller NJ home and investment assets, it diversifies beyond real estate and begins generating income rather than requiring it.

Whatever the deployment strategy, the key insight is this: the wealth is real. The decision about what to do with it deserves the same level of care and intentionality that went into building it — even though building it required nothing more than paying the mortgage every month and staying.

FAQ

Is Bergen County real estate a better investment than the stock market? Over long holding periods with leverage factored in and housing services included, Bergen County homeownership has been competitive with — and in some periods better than — stock market returns for many families. The comparison is complex because the investments are structurally different. Homes are illiquid, leveraged, require maintenance, and provide direct utility. Stocks are liquid, easily diversified, and require no upkeep. Most financial advisors suggest owning both rather than choosing one.

How much of Bergen County home appreciation is inflation vs. real return? A meaningful portion of nominal home price appreciation is inflation — homes are priced in dollars, and dollars have lost purchasing power over 30 years. The real (inflation-adjusted) appreciation of Bergen County homes is lower than the nominal number. However, because mortgages are fixed in nominal dollars, inflation benefits the leveraged homeowner: you pay back the loan in inflated dollars while the asset holds real value. This is one of the structural advantages of leveraged residential real estate as an inflation hedge.

What are the tax implications of selling a home that has appreciated significantly in Bergen County? The federal capital gains exclusion shelters $250,000 (single) or $500,000 (married) of gain on a primary residence sale. For a Bergen County homeowner with $700,000 in total appreciation, a married couple would shelter $500,000 of that gain from federal capital gains tax and pay tax only on the remaining $200,000. New Jersey conforms to the federal exclusion. Gains above the exclusion are taxed at applicable capital gains rates. A tax professional should be consulted before making any sale decision on a long-held, highly appreciated property.

Your Equity Has a Next Act

The wealth you've built in Bergen County over 30 years is not an accident. It's the result of a commitment — to a community, to a mortgage, to a piece of land on the most valuable stretch of real estate adjacent to the most powerful city in the world.

What happens to that wealth next is a decision worth making carefully.

Scott Selleck, REALTOR® with The Selleck Group at KW City Views Realty, has helped Bergen County homeowners understand and deploy their equity for 34 years. If you're beginning to think about what the next chapter looks like, start with a conversation about what you're actually holding — and what it could do.

Call or text 201-970-3960 | [email protected] | SelleckSellsNJ.com

This post is for informational purposes only and does not constitute financial or tax advice. Consult qualified professionals for guidance specific to your situation.