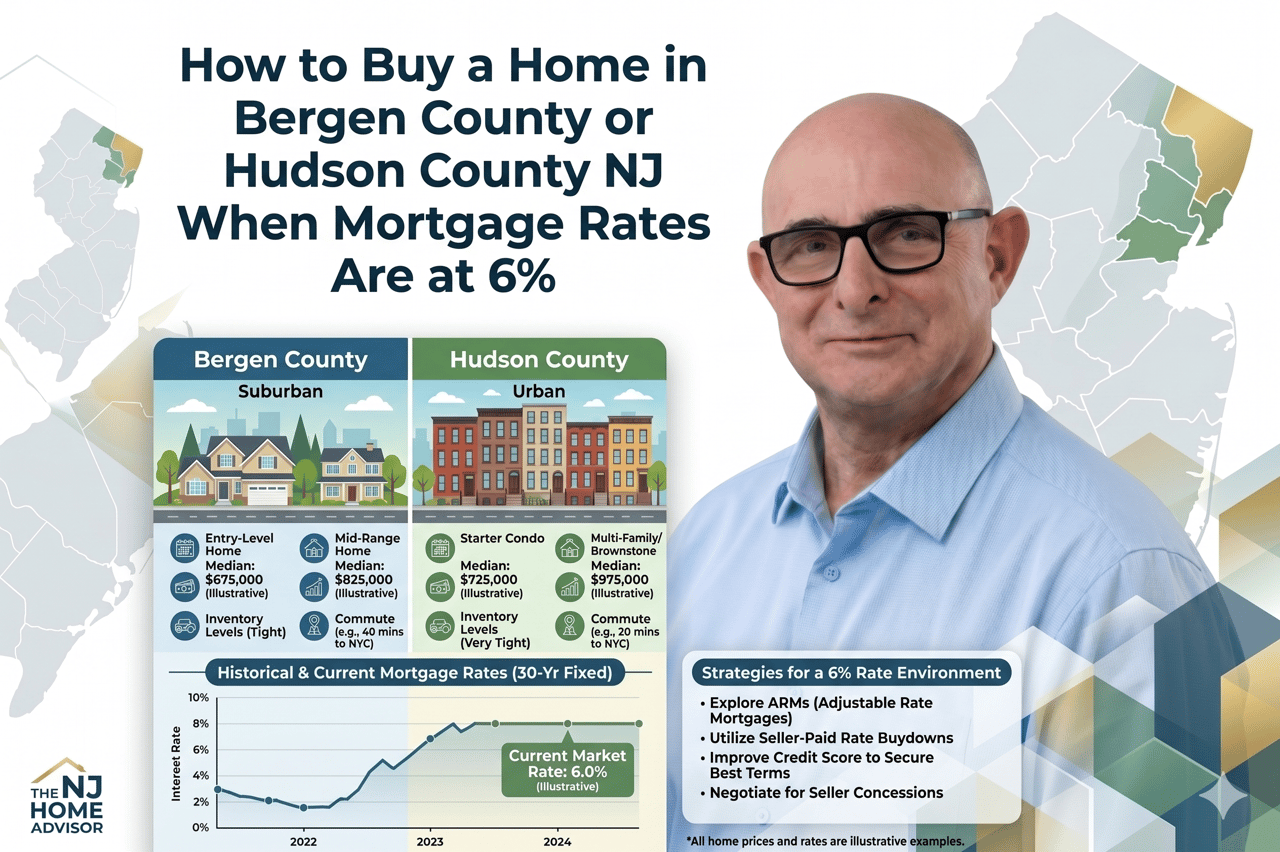

Exploring Different Mortgage Options and Finding the Best Fit in Bergen County

What mortgage options should you explore when buying a home in Bergen County—and how can you find the best fit for your goals?

Buying a home is one of the biggest financial decisions you’ll ever make, and choosing the right mortgage is just as important as finding the right property. With Bergen County’s diverse housing market—ranging from condos and townhomes to luxury single-family homes—understanding your financing options helps you make confident, informed choices.

Here’s a breakdown of the most common mortgage types and how to decide which one works best for you.

Conventional Loans: The Classic Choice

Best for: Buyers with good credit and stable income

Conventional loans are the most common type of mortgage. They typically require:

-

A minimum credit score of 620 or higher

-

Down payments as low as 3% (though 20% avoids PMI)

-

Flexible terms from 15 to 30 years

These loans aren’t backed by the government, giving lenders flexibility and borrowers more options. They’re ideal if you’re financially strong and looking for competitive interest rates.

FHA Loans: A Great Option for First-Time Buyers

Best for: Buyers with moderate credit or limited savings

Backed by the Federal Housing Administration, FHA loans are designed to make homeownership accessible. They feature:

-

Down payments as low as 3.5%

-

More lenient credit requirements

-

Fixed interest rates and longer loan terms

FHA loans are popular among first-time buyers in Bergen County who need a little extra flexibility to get started.

VA Loans: A Powerful Benefit for Veterans

Best for: Active-duty military, veterans, and eligible spouses

The VA loan, backed by the U.S. Department of Veterans Affairs, offers incredible benefits:

-

No down payment required

-

No private mortgage insurance (PMI)

-

Competitive interest rates

If you qualify, this can be one of the most affordable paths to homeownership in New Jersey.

USDA Loans: For Rural and Suburban Buyers

Best for: Buyers in eligible rural or suburban areas

The USDA loan, backed by the U.S. Department of Agriculture, helps buyers in qualifying areas purchase homes with:

-

Zero down payment

-

Low fixed rates

-

Income-based eligibility

While Bergen County is mostly suburban and urban, parts of nearby counties may qualify—so it’s worth checking if you’re open to exploring the outskirts.

Adjustable-Rate Mortgages (ARMs): Flexibility for Short-Term Plans

Best for: Buyers planning to move or refinance within a few years

ARMs start with a low introductory rate that adjusts after a set period. They can be a smart short-term strategy, especially if you plan to relocate or refinance before the rate changes.

Just be sure you’re comfortable with potential fluctuations in monthly payments later on.

Finding the Right Fit

Choosing a mortgage isn’t just about the lowest rate—it’s about aligning with your lifestyle, goals, and financial comfort.

Here’s how to narrow it down:

-

Review your long-term plans. How long do you expect to stay in the home?

-

Consider your down payment flexibility.

-

Compare lender programs—some offer local first-time buyer incentives.

-

Work with a local expert who understands Bergen County’s market dynamics.

Final Takeaway

Every buyer’s financial picture is unique—and the right mortgage can make homeownership more affordable and sustainable. By exploring all your options and working with trusted professionals, you’ll secure financing that fits your goals today and your future plans tomorrow.

Schedule a Consultation Today

Ready to explore your mortgage options in Bergen County? I can help connect you with trusted local lenders and guide you through every step of your home-buying journey.

📞 Call Scott Selleck of The Selleck Group, KW City Views Realty at 201-970-3960 or email [email protected] to get started.