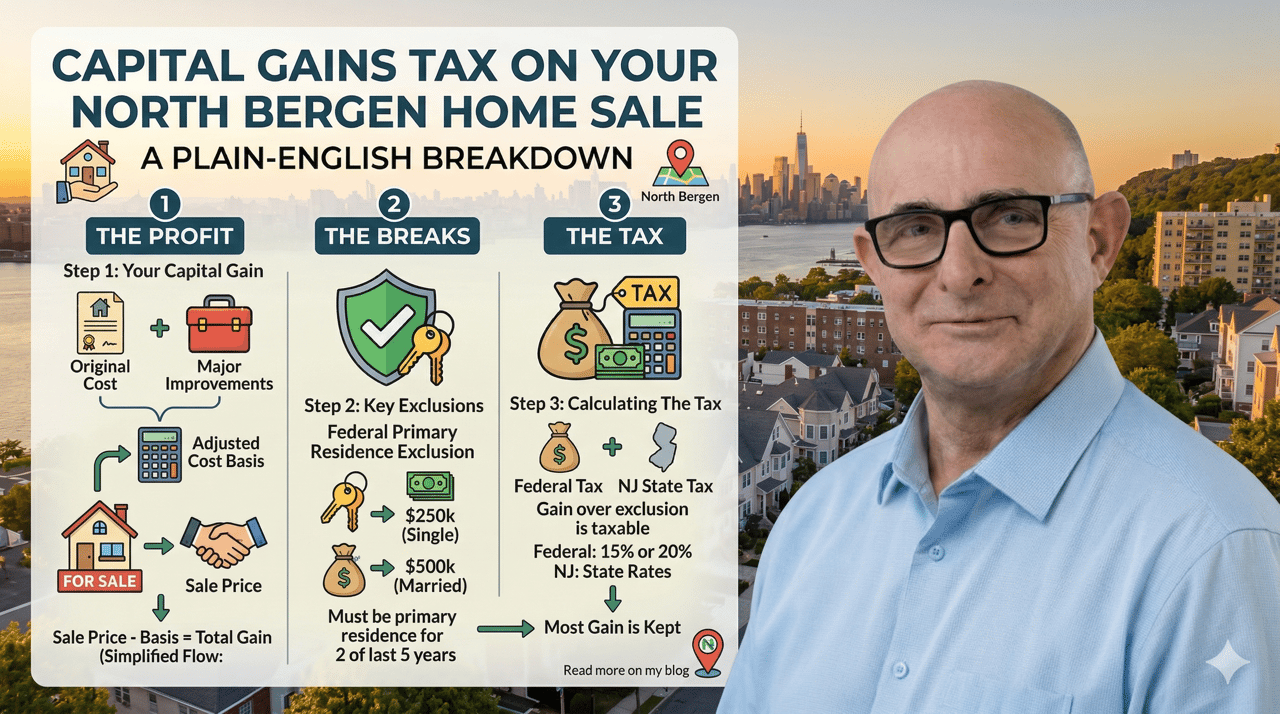

Capital Gains Tax on Your North Bergen Home Sale: A Plain-English Breakdown

Do I owe capital gains tax when I sell my North Bergen home? Most North Bergen homeowners who've lived in their property as a primary residence for at least two of the last five years qualify for the federal primary residence exclusion — up to $500,000 in gains tax-free for married couples — but New Jersey taxes gains as ordinary income on top of that, and the details are worth understanding before you list.

North Bergen doesn't generate the same real estate headlines as its neighbors to the south. But the equity story here is real.

Homeowners who purchased in North Bergen's established residential blocks in the 1990s or early 2000s have seen consistent appreciation driven by the borough's commuter value, its Palisades positioning, and the steady northward migration of buyers from more expensive Hudson County markets.

That appreciation has built meaningful equity for a lot of families who stayed put and didn't think much about it year to year.

When it's finally time to sell, the capital gains question surfaces quickly. And for most North Bergen sellers, the answer is better than they expect, as long as they understand the framework before they get to the closing table.

This is not tax advice. A CPA should review your specific situation before you close. But here's what every North Bergen seller should know going in.

The Most Important Distinction: Gain vs. Sale Price

Most sellers conflate these two numbers and end up overestimating what they owe.

Capital gains tax is not applied to your total sale price. It is applied to your profit.

Your profit is your sale price minus your adjusted cost basis. That basis starts with your original purchase price, increases with qualifying capital improvements made during your ownership, and includes certain closing costs from the original transaction.

A North Bergen homeowner who paid $280,000 for a single-family home in 1999 and sells today for $580,000 has a $300,000 gain before any improvement adjustments. The tax calculation works from $300,000, not $580,000.

That reframing changes the conversation for most sellers before the exclusion even comes into play.

The Federal Primary Residence Exclusion

The Section 121 exclusion is the central protection available to North Bergen sellers.

Own your home and use it as your primary residence for at least two of the last five years before the sale, and you can exclude up to $250,000 in capital gains from federal income tax as a single filer. Married couples filing jointly can exclude up to $500,000.

For a North Bergen couple with a $300,000 gain and a $500,000 exclusion, the federal capital gains tax is zero.

That outcome is common in North Bergen's mid-range residential market, where long-term owners have built real equity but typically haven't seen the kind of extreme appreciation that pushes gains dramatically past the exclusion threshold.

The exclusion has conditions though, and a handful of situations can reduce or eliminate it.

When North Bergen Sellers May Still Owe Federal Tax

Your gain exceeds the exclusion. North Bergen's Palisades ridge properties with Manhattan views have seen stronger appreciation than the township's interior blocks. Long-term owners in those corridors can find themselves with gains approaching or above the $500,000 married threshold. The amount above the exclusion is taxable at long-term capital gains rates: 0, 15, or 20 percent federally depending on your income.

You haven't met the two-year residency test. If you've rented the property, recently moved in before selling, or used it as a second home rather than a primary residence, your timeline may not qualify. Partial exclusions are available in specific circumstances tied to job changes, health issues, or other unforeseen events, but the rules are narrow.

You've used the exclusion within the past two years. The Section 121 exclusion can only be claimed once every two years. A recent sale of another primary residence may affect your eligibility.

You rented the property and claimed depreciation. If you rented your North Bergen home at any point and took depreciation deductions on your tax returns, the IRS requires recapture of that accumulated depreciation at a flat 25 percent federal rate at closing. This applies regardless of whether the rest of your gain qualifies for the exclusion and catches sellers off guard more often than any other tax item in this conversation.

New Jersey's Treatment — The Layer Most Sellers Miss

Federal tax is only half the picture.

New Jersey taxes capital gains as ordinary income. Any gain above your federal exclusion gets added to your regular NJ taxable income for the year of the sale and taxed at your marginal NJ rate.

New Jersey's income tax brackets run from 1.4 percent at the low end to 10.75 percent for income over $1 million. Most North Bergen sellers with a meaningful gain above the federal exclusion will land in the 5.525 to 8.97 percent range on that amount.

There is no NJ equivalent of the federal primary residence exclusion. The federal exclusion reduces your federal liability. It has no effect on your NJ liability for the same amount.

For a North Bergen seller with $75,000 above the federal exclusion, the combined federal and NJ tax bill on that amount could run $15,000 to $25,000 depending on income. That's a number worth knowing before you're under contract, not after.

The NJ Realty Transfer Fee

Separate from capital gains, every New Jersey home sale carries a Realty Transfer Fee paid by the seller at closing. It is calculated as a percentage of the sale price and scales upward for higher-value transactions.

It is not a capital gains tax. But it reduces your net proceeds and belongs in your pre-sale financial planning alongside the tax picture.

The Exit Tax for North Bergen Sellers Moving to Florida

For North Bergen homeowners planning a transition to South Florida, the NJ exit tax is a closing-day cash flow item that surprises sellers who don't plan for it.

If you've established Florida residency before your North Bergen closing, New Jersey requires an estimated income tax withholding at closing. The withholding is the greater of 8.97 percent of the gain or 2 percent of the sale price.

It is a prepayment against your final NJ tax liability, not an additional tax. You get credit for it when you file your NJ return. But on a $550,000 North Bergen sale with a significant gain, that withholding can run $11,000 to $50,000 at the closing table depending on the numbers.

The Selleck Group builds this into every NJ to FL transition plan so it is never a surprise. Knowing the number in advance changes how you plan the Florida purchase and what cash you have available after closing.

How Capital Improvements Work in Your Favor

Every dollar you've invested in qualifying capital improvements to your North Bergen property increases your adjusted cost basis and reduces your taxable gain.

Qualifying improvements for a single-family home typically include a new roof, kitchen renovation, bathroom addition or remodel, finished basement, HVAC replacement, new windows, room additions, and similar permanent upgrades. Routine maintenance, painting, and minor repairs generally don't qualify.

For a North Bergen homeowner who has invested $40,000 to $80,000 in improvements over 20 years of ownership, that documentation directly reduces the gain subject to tax.

The challenge is always records. Contractor invoices, permit applications, and receipts from work done a decade ago aren't always organized or easy to find. Start pulling whatever you have before your CPA meeting. Partial documentation is worth more than nothing.

Three Steps to Take Before You List

Step one: Get a current CMA. Know your likely sale price before any tax planning conversation begins. The Selleck Group provides this at no cost to North Bergen homeowners. Your projected sale price combined with your adjusted cost basis gives your CPA the inputs needed to model the full tax picture accurately.

Step two: Reconstruct your adjusted basis. Pull your original purchase documents, your HUD-1 or closing disclosure from when you bought, records of capital improvements, and prior tax returns if you've ever rented the property. Your CPA needs all of it.

Step three: Meet with a CPA before you list. Not after you accept an offer. The earlier you have the tax picture, the more planning options you have, including timing decisions that affect which tax year the gain lands in and how your residency status affects NJ exposure.

FAQ

I've owned my North Bergen home for over 20 years. Does the length of ownership affect my capital gains rate? Indirectly, yes. The long-term capital gains rate, which is lower than ordinary income rates, applies to any property held for more than one year. Almost all North Bergen long-term owners qualify automatically. The rate itself is 0, 15, or 20 percent federally depending on your total taxable income for the year. Length of ownership beyond one year doesn't change the rate further, but it does mean the lower long-term rate applies rather than the higher short-term rate.

What if my North Bergen home has a separate apartment that I've been renting out? This is a common situation in North Bergen's multi-family and mixed-use properties. The portion of the home used as a rental is treated differently from the owner-occupied portion for both the primary residence exclusion and depreciation recapture purposes. The allocation between personal use and rental use affects how much of the gain qualifies for the exclusion and how much depreciation must be recaptured. A CPA should model this before you list.

Is there any benefit to waiting until next year to sell my North Bergen home for tax purposes? Possibly, depending on your other income. If your income will be significantly lower next year due to retirement, reduced earnings, or other factors, the capital gains rate on any amount above the exclusion may be lower in that year. Your CPA can model both scenarios with real numbers to determine whether the tax savings justify the timing change given current market conditions.

Ready to make a move? Scott Selleck, REALTOR® with The Selleck Group at KW City Views Realty, works with North Bergen and Hudson County homeowners through every stage of the selling process, including the financial planning conversations that happen before the listing goes live. Get your no-cost CMA and a clear picture of your equity position today. Call or text 201-970-3960 or visit www.SelleckSellsNJ.com.